Last week, I argued that the Federal Reserve had not made a communication error when it announced in its June FOMC statement that it would begin tapering later in the year if the economy continued to improve at a moderate pace. The problem was that the market did not listen to the Fed correctly. The Fed’s non-taper was not to correct a miscommunication. It was to correct the market’s misreading of that statement. That’s not to say that the Fed’s policies have been optimal. On the contrary, while the Fed did not make a mistake in its communication strategy, its’ making an even worse one in tapering prematurely.

When Ben Bernanke announced that the Fed was going to start a new round of quantitative easing (QE3), the unemployment rate stood at 8.1%. Today, it’s down to 7.3%, but this overstates the extent to which the economy has improved in that time. In particular, workers have dropped out of the labor market at an alarming rate, causing the unemployment rate to drop for the wrong reasons. Some of those workers are baby boomers retiring, but many more are simply people who are so discouraged that they give up looking for a job.

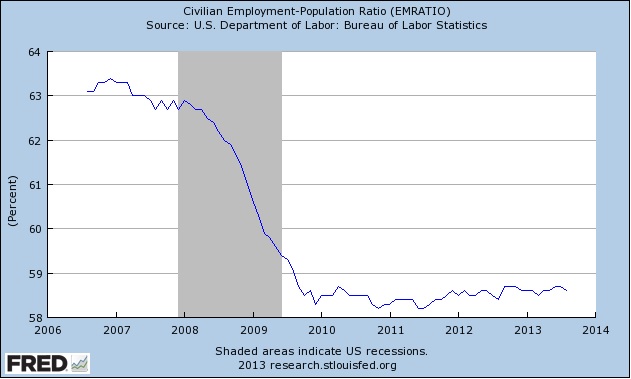

A better indicator of the state of the labor market is the employment-to-population ratio:

.

.

As you can see, the employment-to-population ratio crashed during the Great Recession as millions of workers lost their jobs. Since then, the economy has muddled along. It’s unlikely that we’ll return to a ratio of 63-64% anytime soon, because as the country gets older, we will have fewer working-age Americans. Nevertheless, the current rate of 58.6% is unacceptable. In June, the rate was 58.7%. Before that, the economy was certainly not growing at a quick enough pace for the Fed to begin reducing its pace of bond-buying.

That’s the Fed’s real mistake.

Bernanke should have announced that the Fed would continue its asset purchases until the economy showed substantial, consistent improvement. He should’ve said that the Fed always follows the unemployment rate closely, but would track a number of economic indicators. It would continue its unconventional monetary policy until either inflation began creeping upwards or the economy returned to full employment. In a perfect world, the Fed should implement NGDP targeting, but given that such a policy is not happening anytime soon, the Fed should focus on using its current unconventional policy to provide support for the economy. That means not reducing the rate of asset purchases when the economy is barely improving.

Except that is exactly what the Fed intends to do. That was what Bernanke announced in June. Unfortunately, economic growth over the past three months has been below the Fed’s forecast so it adjusted its policy and delayed tapering. But when the economy does improve more and the Fed decides to taper, it will make a big mistake. The Fed could correct its policy and decide to continue its bond-buying for a longer period of time until the economy grows stronger. But that would be an entirely different message than the one Bernanke delivered in June. Then, the miscommunication criticism would ring true.

However, there are no signs that this will be the case. Everything Bernanke said at this past press conference indicates that the Fed is ready to begin tapering once the economy grows at a slightly faster rate. It’s not a mistake of miscommunication. It’s a policy mistake. And since it’s going to hurt economic growth and weaken an already weak labor market, that’s a much worse mistake to make.