In my class on housing policy today, we spent some time discussing judicial vs. non-judicial foreclosures and the reasoning behind the different processes. I’m a bit new (and a bit behind) to all of this so let’s break it down a bit:

A judicial foreclosure state requires a lender to file a number of documents with the court to kick off the foreclosure process. The homeowner is sent a notice of the filing and receives the opportunity to contest the sale. Judicial foreclosures can drag on for months and are subject to much scrutiny. A non-judicial foreclosure state requires a lender to file a notice of default and notify the homeowner of it as well. The homeowner still can object to the foreclosure and take the matter to court, but otherwise the court is not involved at all. It does not examine any paperwork or scrutinize the foreclosure. This process is much quicker and less costly to lenders.

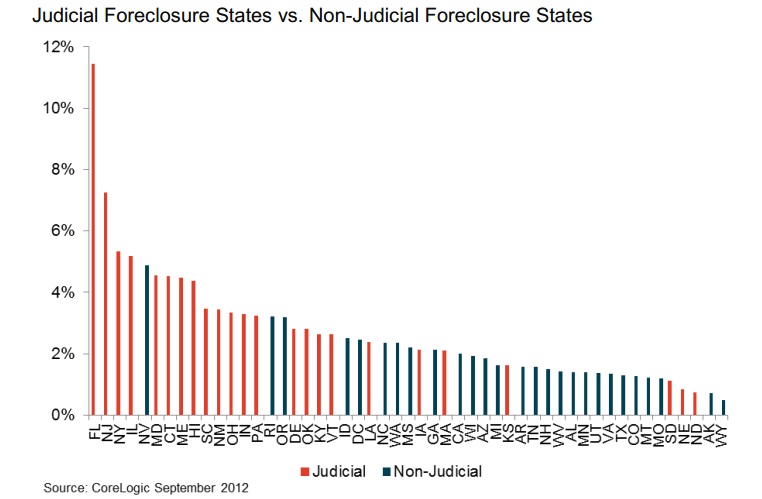

Our conversation in class today was kicked off by the following graph:

The left axis shows the percent of existing mortgages currently in the foreclosure process. Clearly, there are a lot more foreclosures in process in judicial states than in non-judicial states. However, this is just because the process takes so much longer. When the foreclosure process drags on for months, there are bound to be a higher percent of mortgages in the foreclosure process than there are in states where the process takes just weeks. This wasn’t particularly surprising.

The left axis shows the percent of existing mortgages currently in the foreclosure process. Clearly, there are a lot more foreclosures in process in judicial states than in non-judicial states. However, this is just because the process takes so much longer. When the foreclosure process drags on for months, there are bound to be a higher percent of mortgages in the foreclosure process than there are in states where the process takes just weeks. This wasn’t particularly surprising.

We then discussed the reasoning behind judicial vs. non-judicial foreclosures. After all, if judicial foreclosures take longer and are more costly, why even have them? The answer is consumer protection. Over the past few years, we’ve seen a huge amount of foreclosure fraud. In judicial states, the courts inspect all the documents of a foreclosure to try to eliminate as much fraud as possible. In non-judicial states, the courts only inspect all the documents if the borrower contests the foreclosure. That requires the borrower to have enough knowledge of the foreclosure process to notice fraud – something very few borrowers are capable or knowledgeable enough to do.

However, the lenders are the ones who must pay the extra costs of the drawn-out foreclosure process in judicial states and I expect that lenders already include such costs in the rates they charge homeowners. This is just the market acting as it should though. The borrower is effectively paying a bit extra for the consumer protection of the judicial foreclosure process. Most borrowers won’t ever default, but for those who do, a judicial foreclosure could save them their home. Of course, the trade-off only makes sense if the judicial foreclosure process actually does cut down on fraud.

That’s where we left off in class, but I was wondering if there were studies that tested the hypothesis. I would expect to see significantly more fraud in cases with non-judicial foreclosures than in those with judicial foreclosures.

The evidence is a bit unclear. Certainly, many lenders commit mortgage fraud. As a 2007 paper in the Texas Law Review by UC-Irvine law professor Katherine Porter puts it, “mortgage servicers frequently do not comply with bankruptcy law.” Porter’s study examined more than 1700 foreclosures in non-judicial states that were contested by the homeowner. She found frequent abuse by lenders throughout all parts of the process.

A more recent audit found that of 400 foreclosures in San Francisco, almost every single one of them had some sort of violation (Both judicial and non-judicial foreclosures are allowed in California, but judicial ones are rare).

Unfortunately, I could not find a study directly comparing the instances of fraud between judicial and non-judicial foreclosure states. Without such studies, it’s impossible to conclude whether judicial foreclosures prevent fraud, but the current evidence makes me hesitantly believe it does. If anyone knows of other studies, please pass them along.

Because the judicial process takes longer, the housing recovery takes longer as well. If the judicial process isn’t actually cutting down on fraud, then we’re just wasting our time and costing borrowers money. A comprehensive study of mortgages in various states over the past few years would do wonders towards answering that question.